Retirement Transition Blueprint: Your Path to a Confident Retirement

Serving Families in Davis County and the Salt Lake Valley

Why You Need a Blueprint

You only retire once — but the decisions you make in those early years will shape the rest of your life. For decades, you’ve been in accumulation mode, saving diligently, investing, and building accounts. But retirement requires a completely different mindset.

This is where many families stumble. Without a system, retirees either:

Leave too much in cash and lose growth potential.

Take on too much risk and get exposed in downturns.

Overspend without realizing how quickly assets can shrink.

Underspend because of fear, leaving money unused and opportunities missed.

The Retirement Transition Blueprint was designed to solve this. It’s a clear, structured system that gives your money purpose, ensures stability, and removes the guesswork from your financial decisions.

The Three Buckets of Retirement Planning

The heart of the Retirement Transition Blueprint is the Three Bucket System. Each bucket has a specific purpose, timeline, and set of “jobs” for your money. Together, they create a coordinated strategy for today, tomorrow, and the decades ahead.

Bucket 1 – Monthly Cash Flow & Emergency Fund

Bucket 1 is where your retirement “paycheck” shows up. Just like when you were working and your salary hit your checking account, this is where income arrives and bills get paid.

Holds your emergency fund — liquid cash you can access immediately when life happens.

Receives your monthly income streams such as pensions and Social Security.

If there’s a gap between your guaranteed income and your actual expenses, we create a predictable monthly “paycheck” by sending money from Bucket 2 into Bucket 1.

This bucket is not about investing — it’s about stability and access. With your emergency cushion in place and your monthly cash flow organized, you can cover expenses and handle surprises without stress.

Bucket 2 – Stability, Income & Fun

Bucket 2 is the shock absorber of your plan. It holds your mid-term money (1–10 years) and keeps you protected from being forced to sell long-term growth assets in a down market.

Pays out a predictable income stream to Bucket 1 each month.

Provides flexibility to fund discretionary spending — travel, hobbies, remodels, or a second home.

Serves as your down-market protection, giving you access to cash even when markets are volatile.

Think of Bucket 2 as your stabilizer. It gives you the freedom to enjoy retirement knowing your short-term income is secure, no matter what’s happening in the markets.

Bucket 3 – Opportunity

Bucket 3 is your long-term opportunity bucket — designed for money you won’t need for 10+ years. This is where you position your wealth to grow, protect against inflation, and fund big-picture goals.

Within the Opportunity Bucket, money can be assigned to specific jobs:

Growth – Investing for the long term to extend the life of your wealth.

Tax Strategy – Using tools like Roth conversions or charitable giving to minimize lifetime taxes.

Healthcare – Preparing for medical costs and potential long-term care.

Legacy – Funding gifts for children, grandchildren, or charitable causes.

By keeping these dollars invested and purposeful, you give them time to multiply — while making sure they’re directed toward the priorities that matter most to you and your family.

The Bucket Refill System

Buckets aren’t static. They’re designed to flow into each other like a well-managed reservoir system.

Bucket 1 is refilled regularly from Bucket 2.

Bucket 2 is refilled from Bucket 3, especially during strong markets.

Regular rebalancing ensures each bucket stays at the right level, aligned with your goals.

This refill process ensures that your daily cash flow is always secure, your mid-term needs are covered, and your long-term money continues to grow. It also removes the stress of deciding “where to pull from” — the system makes that clear.

The Four Pillars of the Blueprint

While the Three Buckets are the structure, the Four Pillars provide the foundation. These are the core areas we focus on when building and maintaining your plan.

Income

Replacing your paycheck with reliable income streams — Social Security, pensions, and structured withdrawals.

Assets

Assigning your accounts to the right buckets, so each has a clear role in supporting your plan.

Goals

Your unique vision for retirement — whether that’s travel, family, service, or leaving a legacy.

Taxes

Your unique vision for retirement — whether that’s travel, family, service, or leaving a legacy.

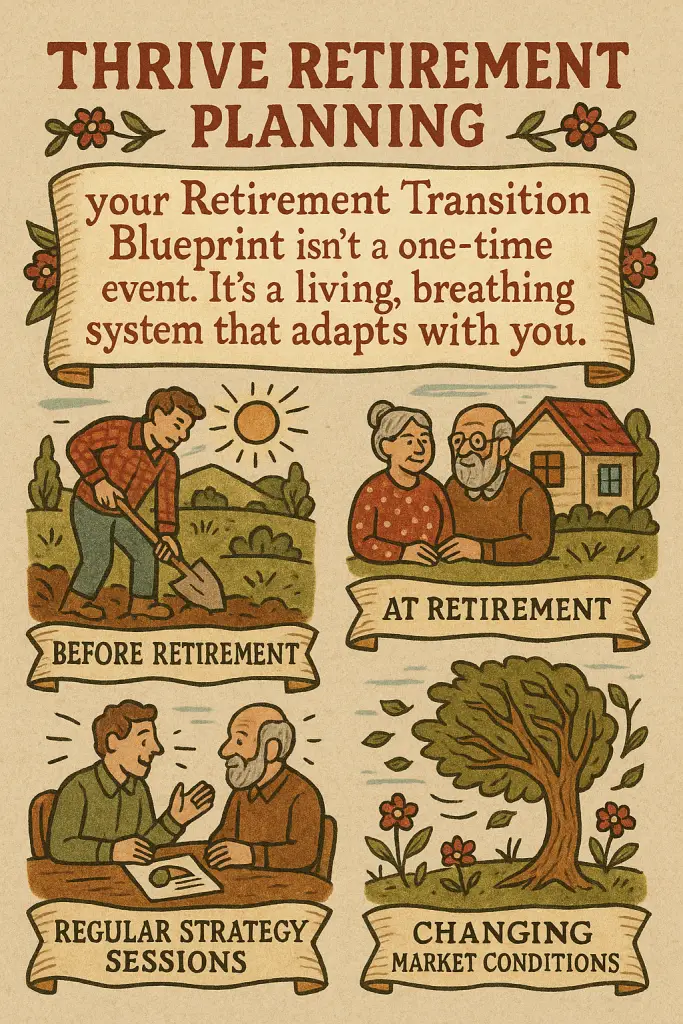

How It Works in Practice

When you work with Thrive Retirement Planning, your Retirement Transition Blueprint isn’t a one-time event. It’s a living, breathing system that adapts with you.

Before retirement: We assign assets to the right buckets in advance, so you’re prepared to retire on your timeline — not forced by market downturns or external events.

At retirement: We finalize your income plan and allocate resources to support your lifestyle from day one.

Each year: We review your plan, rebalance, and refill buckets as needed.

In down markets: Bucket 2 protects your lifestyle, so you’re not forced to sell growth assets at a loss.

In good markets: Gains from Bucket 3 replenish Bucket 2, extending your stability.

This system keeps you steady through ups and downs. Instead of reacting emotionally, you follow a disciplined plan — one that’s built to last.

Why Families in Davis County and the Salt Lake Valley Value This Approach

We’ve seen firsthand how powerful the Retirement Transition Blueprint can be for local families.

A couple in Bountiful used the system to finally feel confident about spending on travel. With a clear refill strategy, they knew their “fun” budget wouldn’t compromise their security.

In Kaysville and Farmington, families found peace of mind knowing her Bucket 1 emergency cushion would always be topped up — no more worrying about unexpected expenses.

A widow in Salt Lake appreciates the structure, especially when helping adult children or planning for healthcare.

In communities across Davis County and the Salt Lake Valley, this approach has taken the fear out of retirement and replaced it with clarity and confidence.

What Our Clients Say

See more reviews on our Testimonials page

Ready to Build Your Retirement Transition Blueprint?

Retirement is too important to leave to chance. With the Retirement Transition Blueprint, you’ll know exactly how your money is working, how your lifestyle is supported, and how your future is protected.

At Thrive Retirement Planning, we specialize in guiding families through this transition. Let us help you create a Blueprint that gives you clarity, confidence, and peace of mind.

Get Started today and begin building your Retirement Transition Blueprint

Thrive Retirement Planning provides retirement planning in Davis County and the Salt Lake Valley using the Retirement Transition Blueprint. Through our proven Three Bucket System, we help families retire with clarity, confidence, and purpose.